Indian banks are now properly positioned to achieve out to offshore shoppers which have, hitherto, most well-liked the NDF market. Initial volumes within the NDF markets have been nearly completely in the interbank section and with restricted counterparties. This was not sudden as banks in India have counterparty limits in place with only a few overseas entities. Client inertia in moving from offshore to onshore markets is steadily waning and some curiosity from global corporates and funds is already seen. As a bigger number of Indian banks start participating actively within the NDF market, they may additionally present an impetus for INR trades to maneuver out of offshore centres both to the onshore market as properly as to the IFSC.

The exchange is going down between the U.S. greenback and won, South Korea’s forex. With an NDS, it isn’t the case as a outcome of the currencies aren’t convertible. The two currencies which are involved within the swap can’t be delivered; hence it’s a non-deliverable swap.

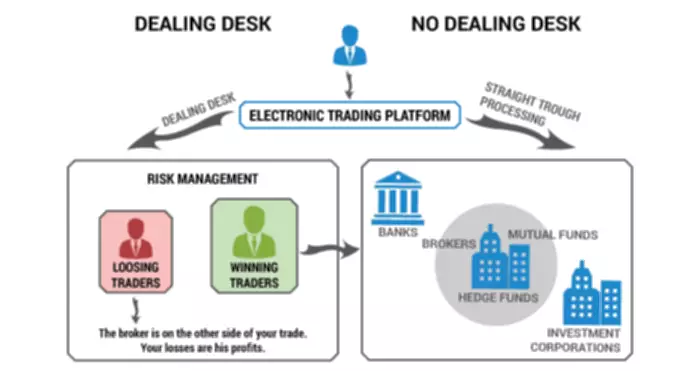

What’s The Difference Between A Foreign Money And Rate Of Interest Swap?

Pay consideration to the trading hours of the NDF market, as it might differ from different monetary markets. The first step in buying and selling NDFs is to find a respected broker who focuses on these monetary instruments. A reliable dealer will offer you the necessary tools and sources to commerce NDFs successfully.

NDF and NDS are both forms of spinoff contracts that allow buyers to trade in currencies that are not freely traded. Non-deliverable ahead (NDF) is a cash-settled contract, which implies that the 2 parties to the contract don’t really exchange the currencies. Instead, they settle the contract in money on the predetermined change price on the settlement date. Non-deliverable swap (NDS) is a physically settled contract, which implies that the 2 parties to the contract actually change the currencies on the settlement date.

Speculative Buying And Selling Alternatives

Korea permitted participation of local banks in the NDF market as a end result of which KRW NDF obtained intently built-in with the onshore markets. The Korean authorities additionally liberalised the onshore KRW market with measures, which abolished approval necessities What Is a Non-Deliverable Forward for some capital account transactions. With the liberalisation of the onshore FX market and the event of a deliverable offshore market (CNH), volumes in the Chinese Yuan (CNY) NDF market have tapered off considerably.

Traders should ensure compliance with all related regulatory necessities to keep away from any legal or operational issues. CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™ certification program, designed to remodel anybody right into a world-class financial analyst. Upgrading to a paid membership provides you entry to our in depth collection of plug-and-play Templates designed to power your performance—as well as CFI’s full course catalog and accredited Certification Programs. The Thai government has strict capital controls in place that make it troublesome for foreigners to purchase and sell THB.

- NDFs can be utilized to create a foreign forex loan in a foreign money, which will not be of interest to the lender.

- In the fast-paced world of financial trading, NDFs (Non-Deliverable Forwards) have emerged as a useful device for traders seeking to navigate the risky currency markets.

- Non-deliverable currencies (NDFs) are a kind of derivative contract that enables buyers to trade in currencies that aren’t freely traded.

- If one celebration agrees to purchase Chinese yuan (sell dollars), and the other agrees to purchase U.S. dollars (sell yuan), then there’s potential for a non-deliverable forward between the two events.

- The settlement date and calculation of NDF contracts are based mostly on the difference between the agreed-upon change price and the prevailing spot price on the worth date.

One of the distinctive options of NDFs is the settlement date and calculation methodology. Unlike traditional foreign money buying and selling, the place physical supply of the underlying currencies takes place, NDFs are cash-settled contracts. This signifies that on the settlement date, the difference between the agreed-upon exchange price and the prevailing spot fee is settled in money. A Non-Deliverable Forward (NDF) is a by-product contract used primarily within the foreign trade (forex) market. They are sometimes utilized in countries with capital controls or where the currency is restricted to hedge against foreign money volatility. When making a settlement between the two currencies involved, worth relies on the spot rate and the exchange fee listed in the swap contract.

Hedging Currency Danger

When trading NDFs, two events enter into a contract that specifies the notional quantity, currency pair, settlement date, and exchange rate. It is necessary to notice that NDFs are traded over-the-counter (OTC), meaning they don’t appear to be traded on a centralized change. NDF stands for Non-Deliverable Forward, which is a by-product instrument used to commerce currencies that are not freely convertible. Unlike conventional foreign money trading, where bodily supply of the underlying forex takes place, NDFs are settled in money. Market volatility refers to the diploma of price fluctuation out there. NDFs are primarily traded in emerging markets, which are inclined to exhibit larger levels of volatility compared to more established markets.

As these markets proceed to develop and achieve significance within the global economy, trading NDFs permits merchants to take part of their growth and capitalize on their potential. This could be notably advantageous for traders in search of diversification and better returns. The settlement date for NDFs is often a specific variety of business days after the commerce date. This allows market participants to hedge their foreign money publicity with out the need for physical delivery. The calculation of the settlement amount takes under consideration the notional amount, agreed-upon exchange price, and the prevailing spot fee on the settlement date. A non-deliverable forward (NDF) is a straight futures or forward contract, where, much like a non-deliverable swap (NDS), the parties concerned set up a settlement between the leading spot fee and the contracted NDF price.

By finding a reliable broker, opening an account, and inserting well-informed trades, you probably can take part on this dynamic market and reap the benefits of the alternatives it presents. NDF contracts come in different sizes and tenors, offering flexibility to traders with varying threat appetites and investment horizons. The contract dimension refers again to the notional amount of the NDF, which represents the underlying quantity of forex being exchanged. It is essential to note that traders are not required to carry the total notional amount to participate in NDF buying and selling.

Traders who anticipate future movements in rising market currencies can take positions in NDFs to doubtlessly profit from those movements. This permits for higher flexibility and access to a wider range of buying and selling alternatives. This also provided opportunities for domestic banks to entry a larger international clientele, together with by leveraging on their abroad department networks. Transaction information indicate that liquidity was starting to build up in particular time buckets within the onshore market, especially earlier than opening and post market closure, before COVID-19 struck (Charts 10 and 11).

Because NDFs are traded privately, they’re a half of the over-the-counter (OTC) market. It permits for extra flexibility with phrases, and since all phrases have to be agreed upon by each parties, the end result of an NDF is mostly favorable to all. Importantly, an onshore interbank NDF market has emerged whereby native banks transact with each other. The participation of Indian banks within the NDF market has increased avenues for interbank threat administration and, going forward, could help convey down hedging cost for purchasers. In New York, the NDFs of BRL have the very best turnover adopted by KRW, Chilean Peso (CLP) and INR (Chart 3).

The largest NDF markets are in the Chinese yuan, Indian rupee, South Korean gained, new Taiwan dollar, and Brazilian real. The largest segment of NDF buying and selling takes place in London, with energetic markets additionally in Singapore and New York. Some countries, including South Korea, have restricted but restricted onshore forward markets along with an energetic NDF market.

Several banks have started participating in the INR NDF markets since then. The average day by day turnover by banks in India8 in the non-deliverable derivative contracts (forwards and options) presently stands at USD 1.1 billion9, with the highest volume of USD 2.97 billion recorded on July 7, 2020 (Chart 14). While Indian banks transact in each non-deliverable ahead and choice contracts, ahead contracts thus far dominate with a share of 97 per cent in complete turnover, most contracts being short tenure contracts of maturity of a couple of week (Chart 15). Concerns about growing NDF volumes have led authorities in several jurisdictions deploying distinct methods.

Longer tenors provide merchants with the chance to take a position on exchange price movements over an extended interval, while shorter tenors permit for more frequent buying and selling alternatives. When trading NDFs, it’s essential to remain informed in regards to the regulations within the particular markets where the trades are carried out. This contains understanding the reporting obligations, capital necessities, and any restrictions on trading activities. By staying abreast of the regulatory landscape, merchants can guarantee they function within the boundaries set by the authorities and decrease the chance of non-compliance. Traders should carefully assess the potential impact of market volatility on their NDF positions.

In the swap, the contract comes with a fixed rate that’s been taken immediately from the spot fee. The U.S.-based firm is about to pay $150,000; the South Korean company is set to pay $90,000 received. The volumes have been almost entirely concentrated within the interbank segment, although there are indications that curiosity from international funds and corporates is slowly rising (Chart 17). More than half of the turnover has been transacted by Indian financial institution branches in Mumbai or IBUs (Chart 18). Offshore individuals have been primarily positioned in London, Singapore and Hong Kong. First, they permit buyers to commerce currencies that may be exhausting or even unimaginable to trade in any other case.